by Dr. Michael Sklarz*, Dr. Norman Miller** and Katrin Kandlbinder***

November 27, 2017

Download a PDF file of this research paper here.

Introduction

Historically, research has shown that out-of-town home buyers are informationally disadvantaged and therefore pay higher prices compared to in-town buyers. However, with the advent of online housing platforms, a plethora of free information about the housing market is now available. Here we test whether the premium paid by out-of-town buyers has declined over time.[1]

We compare the premiums paid in 2005 those paid in 2015 by out of town buyers. The results support the hypothesis that out-of-town buyers continue to pay higher prices for homes, compared to their local counterparts, and that both search costs and anchoring cause a premium. The premium due to higher search costs seems to have decreased over time. Whether the premium will decline to zero over time seems unlikely given the friction of travel costs and the reliance on agents who understand the impact of higher search costs on out-of-town buyers.

Past Research on Search Costs and Home Prices

Past research has found that out-of-town buyers “overpay” for real estate, compared to local buyers. The reason why out-of-town buyers pay more is twofold. Firstly, local buyers face lower search costs, are better informed and often have more time to search for a new home, and therefore, pay lower prices compared to out-of-town buyers (Clauretie and Thistle, 2007; Lambson et al., 2004; Miller, Sklarz and Ordway, 1988, Miller and Rice, 1981). In one of the first out-of-town empirical studies, Miller, Sklarz and Ordway found a 23 percent premium for Japanese buyers of homes in Hawaii, but attributed much of this to the strong Yen/dollar exchange rate. Some of this premium may have been due to less information and/or asymmetric information exploitation by real estate agents. Secondly, researchers have shown that out-of-town buyers from areas where real estate prices are high, relative to local prices, may have upwardly biased expectations of property values and therefore overpay (Zhou et al., 2015; Ihlanfeldt and Mayock, 2012). This phenomenon is a cognitive bias and has been termed the “anchoring effect” (Tversky and Kahneman, 1974).

Ling et al. (2016) confirmed both reasons, namely that out-of-town buyers pay a premium for real estate due to informational disadvantages and anchoring. They stated that these pricing outcomes are more likely to be observed in segmented and informationally inefficient markets.

Although the effects of different search costs in relation to geographical distance and behavioral bias on pricing outcomes have been documented in the literature, the possible effects from increased information availability in the last few years has not been addressed. Therefore, we address three research questions: (1) Do out-of-town buyers pay more for real estate compared to locals? (2) If so, is that premium caused by different search costs (distance), biased beliefs (anchoring) or the level of personal income (wealth)? (3) Did the search cost premium decrease from 2005 to 2015 due to better public information provided by the internet?

A similar question has already been addressed by Turnbull and Sirmans (1993). They investigated whether existing institutions, like the multiple listing service (MLS) and mortgage lending requirements provide sufficient information to protect less-informed buyers from systematically purchasing houses for more than they are worth. Of course, several subsequent studies have suggested that mortgage lenders do not protect buyers from overpaying which helped to fuel the housing crisis of 2007-2008 in the US. Recent academic literature confirms that appraisal bias and inflation were pervasive among loans originating and sold into RMBS during the 2002-2007 period. According to one of these studies, Griffin and Maturana (2016) examined over three million loans that were sold into non-agency RMBS between 2002 and 2007. With the aid of a retrospective AVM (Automated Valuation Model), the authors found that the appraisals were overstated (by 20% or more) for 13.2% of purchases and 20.5% of refinances, an average of 17.8% of the loans overall. Similar results have been published by Agarwal et al. (2015).

Here, we pursue the original question of Turnbull and Sirmans (1993), but focus strictly on the information-availability side. We aim to find out whether the enormous increase in information availability by the internet over the last 10 years has assisted previously informationally disadvantaged out-of-town buyers by reducing the probability of overpaying.

The reason why we believe it is important to investigate especially the last question, is that there has been an enormous rise in information availability over the last decade. With the launch of home search websites like Realtor.com, Zillow, and Redfin since 2006, a plethora of information about the housing market is now provided for free. For example, the history of past selling prices or time on the market since listing, or price trends in the neighborhood. These websites act as real estate and home-related information marketplaces, empowering homeowners, buyers, sellers, renters, professionals, and lenders of all types with data, and various forms of knowledge about the real estate market. Many of these websites are national covering most homes in the US. By acting as electronic marketplaces, these home search websites tend to equalize the information level between heterogeneous buyers and sellers. If information asymmetry or search costs decrease systematically with an increased availability of information, then the prices paid for comparable properties should be more equal, exhibiting less price dispersion and a lower price premium, and that for all buyer types (Byrnjolfsson and Smith, 2000).

Here we examine whether different categories of homebuyers (out-of-town and in-town buyers) pay significantly different prices for comparable houses, and whether this difference has changed between 2005 and 2015. These two years are chosen, because they constitute a sufficient time gap associated with an enormous improvement in information availability. We use the Miami-Dade market for our analysis where we have the vast majority of all transactions.

By incorporating a sequential-search model, we identify potential price effects with respect to differential search costs and anchoring behavior. The search model can be described mathematically as an optimal search-stopping problem and builds on prior real estate search models such as Zhou et al. (2015), Lambson et al. (2004), Turnbull and Sirmans (1993), and Miller and Rice (1981). In a first step, we introduce the common assumptions of our search model followed by the scenarios of changing search costs and the anchoring effect.

To estimate the effect of search costs, anchoring and wealth on the transaction price, we estimate the value of a property using a multiple regression model described more fully in the academic paper available upon request. We measure out of town based on a distance measure. The further away one lives from the property purchased, the more we assume that information will be more costly to acquire. We also check to see if there is an anchoring effect, based on coming from a more expensive or cheaper market, which may influence the formation of what one thinks a property is worth.

Results

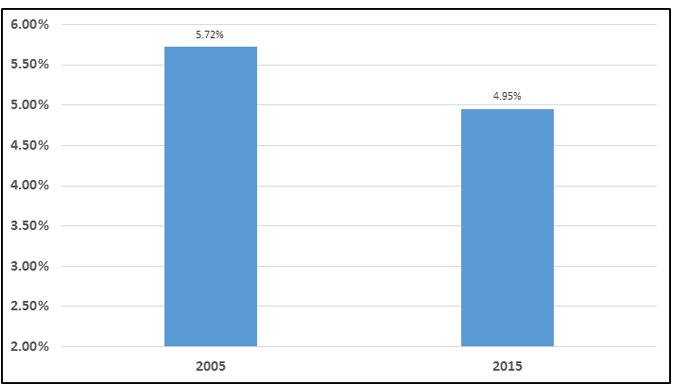

The data used in this paper include public record condominium transactions that occurred in Miami-Dade County in 2005 and 2015. Our overall dataset consists of 15,795 transactions from which 5,446 took place in 2005 and 10,349 in 2015. The out of town premium paid is 2005 averaged 5.72% while the average premium paid in 2015 was 4.95%. This is only a slight decline, which suggests that search costs still matter and that other sources of information may dominate the price paid by buyers. For the mean property value of $275,837 in 2005, the coefficient translates into out-of-town buyer leaving an average of $15,777 on the negotiating table, relative to in-town-buyers if he lives 100 miles away. In 2015, this premium is only $13,939, as shown in Exhibit 1 below.

Exhibit 1: Out of Town Premiums Declining but Remain Significant

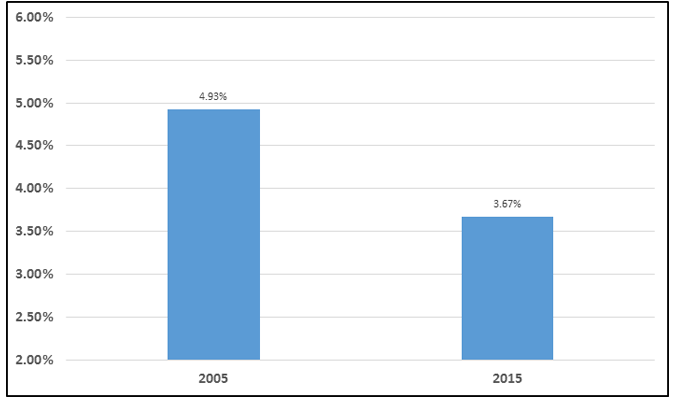

In order to investigate whether buyers pay a premium due to biased beliefs, we enlarge our regression model by an anchor variable, which supposedly induces a premium as well. The coefficients of anchor are positive and statistically significant in both years at 0.0003. This result indicates that buyers from higher priced cities are paying slightly more than buyers from cities with lower housing prices – even if the coefficients are fairly small. The anchoring effect remains at the same level for both years and the out of town premium remains albeit slightly smaller than before, as shown in Exhibit 2.

Exhibit 2: Out of Town Premiums While Controlling for Anchoring Effects

Conclusions

Our results show that distant buyers continue to pay a price premium, relative to local buyers based on extensive data samples from Miami-Dade County in 2005 and 2015. The premium in 2015 is lower than in 2005. This decrease may be due to better public information. Behavioral bias in the form of anchoring (comparing prices to the buyer’s home market) tend to play a less important role, as the anchor premium is statistically significant but very small. We found evidence that the out-of-town buyer premium due to distance decreases by 13.46% from 2005 to 2015. Therefore, the internet likely contributes to equalizing prices paid by out-of-town buyers and locals to some extent, as the premium in 2015 is not as high as in 2005, but real estate remains a far less than perfectly competitive market characterized by price dispersion, high transactions costs and noise. It is also possible that many buyers don’t use the available information and continue to rely on real estate agents as the dominant source of market information.

__________________________

* Collateral Analytics CEO

** University of San Diego and Collateral Analytics Research

*** University of Regensberg PhD Candidate and Visiting Scholar, University of San Diego, 2016-2017

References

Agarwal, S., Ben-David, I. and Yao, V. (2015), “Collateral Valuation and Borrower Financial Constraints. Evidence from the Residential Real Estate Market”, Management Science, Vol. 61 No. 9, pp. 2220–2240.

Clauretie, T.M. and Thistle, P.D. (2007), “The Effect of Time-on-Market and Location on Search Costs and Anchoring. The Case of Single-Family Properties”, The Journal of Real Estate Finance and Economics, Vol. 35 No. 2, pp. 181–196.

Griffin, J.M. and Maturana, G. (2016), “Who Facilitated Misreporting in Securitized Loans?”, Review of Financial Studies, Vol. 29 No. 2, pp. 384–419.

Lambson, V.E., McQueen, G.R. and Slade, B.a. (2004), “Do Out-of-State Buyers Pay More for Real Estate? An Examination of Anchoring-Induced Bias and Search Costs”, Real Estate Economics, Vol. 32 No. 1, pp. 85–126.

Ling, D.C., Naranjo, A. and Petrova, M.T. (2016), “Search Costs, Behavioral Biases, and Information Intermediary Effects”, The Journal of Real Estate Finance and Economics.

Miller, N.G. and Rice, P. (1981), “A Note on the Differentiation of the Market Participants by Search Costs”, Economics Letters, No. 7, pp. 39–46.

Miller, N.G., Sklarz, M.A. and Ordway, N. (1988), “Japanese Purchases, Exchange Rates and Speculation in Residential Real Estate Markets”, The Journal of Real Estate Research, Vol. 3 No. 3, pp. 39–49.

Turnbull, G.K. and Sirmans, C.F. (1993), “Information, search, and house prices”, Regional Science and Urban Economics, Vol. 23, pp. 545–557.

Tversky, A. and Kahneman, D. (1974), “Judgment under Uncertainty: Heuristics and Biases”, Science, Vol. 185 No. 4157, pp. 1124–1131.

Zhang, Y., Zhang, H. and Seiler, M.J. (2016), “The Impact of Information Disclosure on Price Fluctuations and Housing Bubbles: An Experimental Study”, Journal of Housing Research, Vol. 25 No. 2, pp. 171–193.

Zhou, X., Gibler, K. and Zahirovic-Herbert, V. (2015), “Asymmetric buyer information influence on price in a homogeneous housing market”, Urban Studies, Vol. 52 No. 5, pp. 891–905.

Zilllow (2017), https://www.zillow.com/corp/About.htm

[1] This working paper is a summary of an academic paper now under review at the Journal of Housing Research entitled Out-of-town Buyer Premiums in US Housing Markets Over Time.