Decline in Rental Yields Changes the Economics for SFR Investors

Rising US home prices have pushed down rental yields in many single-family rental (SFR) markets, a trend that will likely discourage some institutional investors from buying distressed properties and converting them into rental units. In addition, institutional investors who entered the market early might start selling properties in regions where home prices have sharply appreciated and shift their capital to regions where they can get higher rental yields. Such sales will generally be credit positive for SFR securitization because early principal redemptions will help to build credit enhancement in the transactions. However, they may expose some investors to prepayment risk.

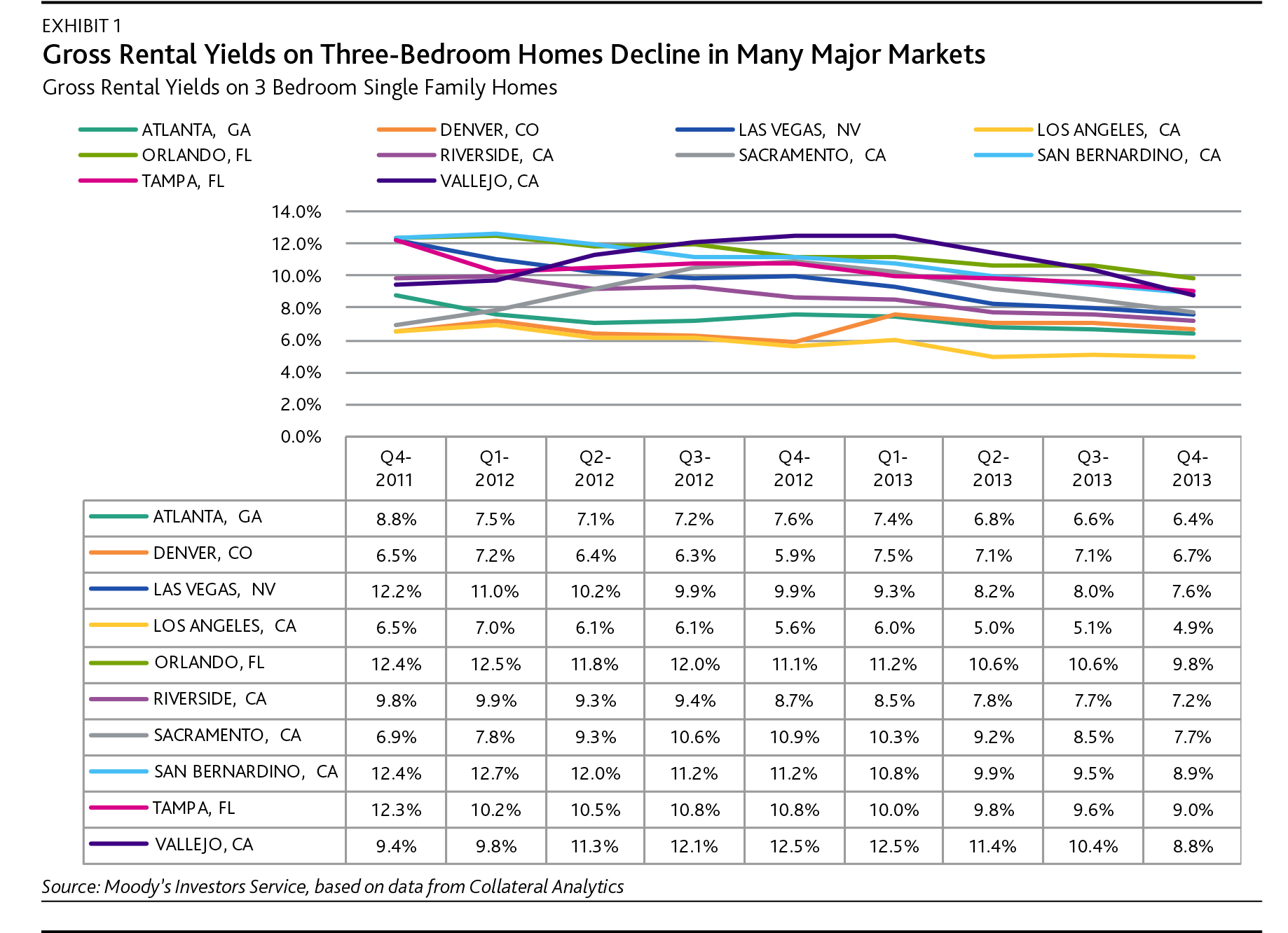

As part of our study, we analyzed a sample of 10 cities* to calculate single-family home rents and implied gross rental yields, defined as the annualized ratio of average monthly rents to home prices excluding operator expenses for property maintenance, on three- and four-bedroom single-family homes from Q4 2011 to Q4 2013. The increase in home prices significantly outpaced the increase in rents during this period, with gross rental yields sliding 20.7% on average for three-bedroom homes across the sample from 9.7% to 7.7%. Rental yields for four-bedroom homes on average declined 18.7% from 8.2% to 6.7%.

Higher home prices are reducing rental yields, making new investments in the SFR market less attractive

Rental yields are falling for SFR properties in prominent markets as a result of steady growth in home prices and stickiness in rents. Exhibits 1 and 2 illustrate gross rental yields for three- and four-bedroom homes in our 10-city sample.

Declining rental yields have several important implications for investors in single-family rentals and for SFR operators. Lower rental yields will pressure rental operators to achieve higher operating effectiveness and cost efficiency to maintain profitability. The impact will be most significant for operators who entered the SFR market recently. For seasoned SFR investors that continue to grow their portfolios, purchases of new and more expensive homes will likely dilute operating income, because lower rental yields would blend with higher yields realized through lower acquisition costs of their earlier purchases. If rental yields are unattractive, fewer investors will purchase homes because their profitability will decline.

Lower rental yields will incentivize SFR investors to rebalance their portfolio

Home price appreciation offers early investors in SFRs an opportunity to rebalance their portfolios of rental properties by disposing of properties in areas with falling rental yields and using the proceeds to purchase properties in other regions where they can get higher yields. Sales of single-family rental properties will generally be credit positive for securitizations backed by those properties, because early principal redemptions will help to build credit enhancement faster and cushion against possible losses. However, early prepayments might expose investors to prepayment risk.

Absolute level of gross rental yields is still attractive given generally low interest rate environment**

Notwithstanding significant declines in gross rental yields in some of the SFR markets, the SFR market will likely continue to attract investor interest. Even with less attractive rental yields, investment in the sector will continue because of the lack of other high-yield investment options. However, investors will be more selective in choosing which regions and properties to acquire.

Increases in home prices across a 10-city sample have significantly outpaced increases in rents, thus decreasing rent yields

We analyzed a sample of 10 cities focusing on trends in single-family home rents and implied gross rental yields on three- and four-bedroom single-family homes. Each city in our sample had an active SFR market. We used home price and rental data provided by Collateral Analytics, whose data sources include public records, current real estate listings and rental advertisements in local media. We excluded two of the active SFR markets, Phoenix, AZ and Houston, TX from our sample because we could not accurately match rental information to key property attributes such as the number of bedrooms in the homes. We selected the time period from Q4 2011 to Q4 2013 to match available home price data with available gross rental yield information.

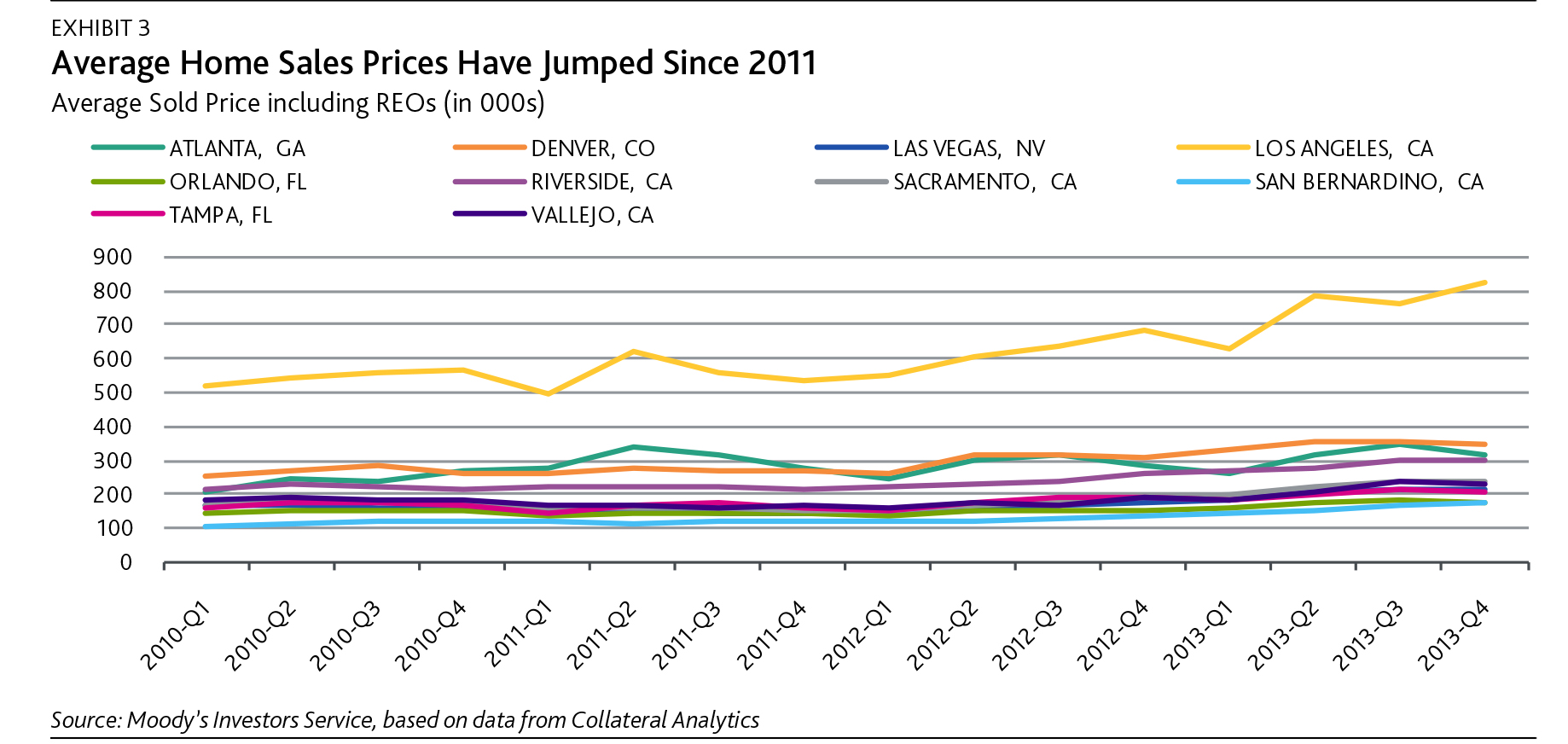

We reviewed trends in the average prices of homes sold that included distressed and non-distressed sales.*** All 10 cities in the sample recorded double-digit increases in home prices, with Las Vegas, NV, Los Angeles, CA and Sacramento, CA posting increases of more than 50%. The average increase across the 10 cities was 38%; excluding Los Angeles, where home prices were significantly higher than in the rest of the sample, the average price of homes sold rose 34%. The pace of price increases has recently moderated, with prices rising approximately 17% on average from Q4 2012 to Q4 2013; excluding Los Angeles, the rate was the same. Exhibit 3 illustrates growth in average prices of homes sold, including distressed sales.

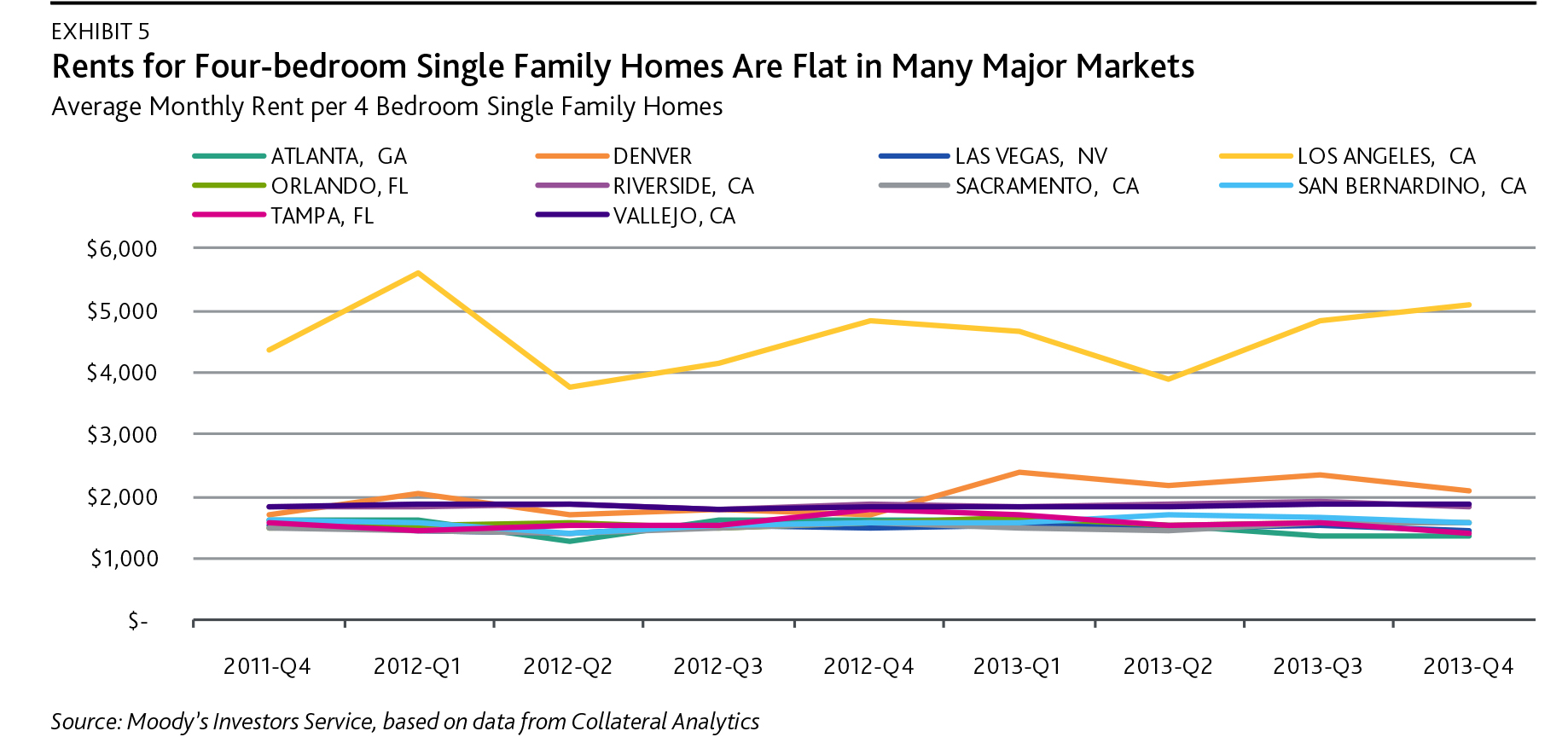

In analyzing rental prices, we reviewed average monthly rents for three- and four-bedroom single-family homes across our sample and compared growth in rents to growth in home prices. We found that the increase in home prices has significantly outpaced the increase in rents, with monthly rents for three-bedroom homes rising 3.3% on average across our sample and rents for four-bedroom homes rising 4.4% on average. Excluding Los Angeles, where rents were materially higher than in the other cities, rents for three-bedroom homes rose 2.2% on average and rents for four-bedroom homes edged up by 0.7% on average.

Denver, CO, recorded the highest growth in rents for three-bedroom homes, followed by Los Angeles, Orlando, FL, and Riverside, CA. For four-bedroom homes, Denver and Los Angeles posted the most notable gains in rental prices, followed by Sacramento and Orlando. Exhibits 4 illustrates average monthly rents for three-bedroom homes and Exhibit 5 depicts average monthly rents for four-bedroom homes.

In evaluating gross rental yield, we base our yield calculation on the quarterly median sold price for all single-family homes in the subject property zip code. For three-bedroom homes, yields declined 20.7% on average across the sample; excluding Los Angeles, yields fell 20.4%. Sacramento and Denver posted increases in gross yields while all other regions recorded declines. Based on the data provided to us, the highest gross rental yields on three-bedroom single-family home rentals across our sample were in Orlando (9.8%), Tampa (9.0%) and San Bernardino, CA (8.9%).

On four-bedroom single-family homes, gross rental yields declined 18.7% on average across the sample, and19.8% excluding Los Angeles. Similar to our analysis of three-bedroom rentals, Sacramento and Denver posted increases in gross yields while yields declined in all other regions. The highest gross rental yields were in San Bernardino (8.6%), Sacramento (8.1%) and Orlando (8.0%).regions recorded declines. Based on the data provided to us, the highest gross rental yields on three-bedroom single-family home rentals across our sample were in Orlando (9.8%), Tampa (9.0%) and San Bernardino, CA (8.9%).

On four-bedroom single-family homes, gross rental yields declined 18.7% on average across the sample, and19.8% excluding Los Angeles. Similar to our analysis of three-bedroom rentals, Sacramento and Denver posted increases in gross yields while yields declined in all other regions. The highest gross rental yields were in San Bernardino (8.6%), Sacramento (8.1%) and Orlando (8.0%).

_________________________________________________________________________

* See Collateral Analytics’ HomePriceTrends January 2014 data.

** As of 25 February, the yield on the 10-year Treasury note was 2.74.

*** We used quarterly data from public records to normalize monthly volatility.

_________________________________________________________________________