Collateral Analytics has developed a new information delivery system to help lenders prioritize the resources devoted to the appraisal process. This new system combines the results of our core AVM products with the results of CA’s new mortgage credit risk model. It builds upon the idea that appraisal errors are more consequential for cases in which the mortgage loan based upon the appraised value is a loan with substantial mortgage credit risk. A simple example of this point is this: a 10-20 percent appraisal error is of little consequence for a loan with an initial LTV of 20 percent in comparison to a loan with a 90 percent initial LTV. Our new information system seeks to highlight those loans with potential appraisal error using existing AVM products combined with information about the mortgage credit risk associated with the loan.

To demonstrate the approach we use AVM information and the credit risk model to identify loans thought to be especially subject to potential appraisal error. For each loan, three measures are available. The first two are standard outputs of CA AVM products. The third is from the credit risk model.

The first is the AVM gap, which is the percentage difference between the AVM and the property value underlying the loan; AVM gap = (AVM – Initial HVAL)/Initial HVAL. Larger “negative” gaps are an indicator that the property is overvalued and, all else equal, the loan based upon the initial appraised value is riskier than the initial appraisal suggests.

The second is the CA Confidence Score. The higher the CA Confidence Score, the more accurate is the initial appraisal. Higher confidence scores are associated with more and better comps for the AVM. Lower confidence scores are associated with more risk to the lender since it raises concerns about the initial appraised value.

The third is a summary measure of the credit risk spread, which is an annualized measure of the projected default costs associated with a loan. The CRS increases predictably with lower borrower credit scores and higher loan to value ratios. A key trait of CA’s CRM is its attempt to incorporate local market conditions that contribute to credit risk. So, for example, a metropolitan area with a more pessimistic forecast of future house prices would have a higher credit risk spread than one with a more optimistic forecast of future house prices.

We can generate this information for any loan submitted to CA.

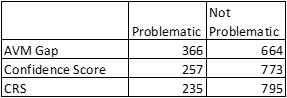

Here are results of a simple case study to demonstrate what we have in mind. We define two categories for each of these three variables: potentially troublesome and adequate. An AVMgap of less than – 50 percent is defined as problematic. A confidence score less than 80 is problematic. The CRS in this example is computed in this example for a loan with an 80 percent LTV and a 700 credit score so the variation in the CRS is driven solely by local market conditions. A problematic CRS for this example is defined to be one in excess of 60 basis points, which is the 75th percentile value of the CRS for the sample of loans.

Here is a simple breakdown of the loans by these three criteria. Of the 1030 loans in the sample for RSFR properties, 366 have a problematic AVM Gap, 257 have a problematic Confidence Score, and 235 have a CRS defined as problematic

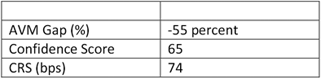

The average values of each of the three criteria for these 51 loans are as follows:

Our report would recommend that these 51 loans receive further attention with either a more comprehensive AVM product, BPO, or a second full appraisal.

Obviously, this example is based upon rather arbitrary notions of problematic. Many other alternatives can be easily constructed. Also, the CRS is based upon a generic prime 30 yr FRM with an 80 percent LTV and a 700 borrower credit score. If more information is available about the loan terms, then the CRS criteria could be defined with the specific traits of the loan. In particular, loans with higher LTVs and lower credit scores would be included in the definition of a problematic CRS.